Why Did Crypto Really Underperform In 2025? The Hard Truths

For most of 2025, the crypto price action felt out of sync with the rest of the risk complex. Equities, gold and even parts of the defense and AI trade found sustained bids, while Bitcoin repeatedly failed to hold breakouts and altcoins bled liquidity.

A widely circulated X post by pseudonymous macro commentator and crypto analyst “plur_daddy” offers one of the most coherent internal diagnoses of what went wrong. His argument is not about a single shock, but about structural supply, fading belief and a new kind of existential risk.

Why Crypto Truly Lagged In 2025

At the core is ownership concentration and the long-awaited six-figure exit ramp. Bitcoin, he argues, “never fully distributed out at lower prices.” Large OG balances accumulated over more than a decade remained tightly held, and 2025 finally offered them both price and liquidity. With spot ETFs, deep derivatives markets and institutional counterparties in place, there was “heavy liquidity available for exiting large bags at the mythical $100k price target,” in line with the long-running meme of “dumping on the suits.”

Around that price region, several narratives converged: the perceived apex of the four-year cycle, a shift in Bitcoin’s image “from being a cypherpunk beacon to a Wall St/Trump family vehicle,” and mounting unease about quantum computing. For holders with essentially their entire net worth in BTC, that mix changed the calculus.

He asks readers to imagine “someone who has massive bags that can’t be sold overnight, with 99.99% of their wealth tied up in a single asset.” Quantum is not cast as an imminent catastrophe, but as a persistent tail risk whose timeline “has been accelerating.” Technical fixes exist, but “they’re all difficult,” and he highlights “the political dysfunction within the Bitcoin dev community.”

Once that worry lodges, he says, “the mind-virus is hard to shake.” With an estimated “$200–250bn+ of OG holdings out there,” it becomes “totally rational to dump a meaningful part of the bag.” In his summary line, “BTC got to a price where the supply overwhelmed the demand in the market.”

The second leg of the underperformance story is narrative. “There wasn’t anything to believe in,” he writes. The meme of financial nihilism may describe reality for some, but “does not captivate the interest of retail buyers.” At the same time, equity markets were selling far more compelling dreams around “AI, quantum, space, drones, nuclear, and defense.”

On the macro-hedge front, “the debasement story for BTC was real but gold simply beat it out.” Bitcoin faced adverse supply dynamics just as gold enjoyed “favorable demand dynamics (Central Bank buying),” weakening BTC’s claim as the superior monetary hedge.

Within crypto itself, there was also a vacuum. In late 2023 and early 2024, the ETFs and then Trump provided powerful, easy-to-grasp narratives. “In 2025,” he argues, “there also wasn’t a narrative around liquidity, or an overarching sense of hope and optimism around what crypto could achieve for the world.”

Liquidity still matters, but in his framing crypto is now “the tip of the spear for liquidity conditions,” a “blow-off valve for excess liquidity.” With conditions “without any doubt” the loosest in 2021 and “meaningfully more loose in 2024 over 2025,” price action simply tracked that tightening.

At the same time, the risk-reward stopped making sense for many participants. BTC “still had a lot of volatility and risk and traded like aids,” he writes, and that was acceptable when the upside was a 3–5x. As people “came to Jesus on the shift in potential upside,” and watched episodes such as the “$10bn seller in July,” they began to question whether trillion-dollar valuations and $500k–$1m BTC really “passed the smell test.”

The internal market structure did the rest. In a “liquidity deprived state,” the game turned increasingly “PvP,” with capital concentrating into sharps who then “offramp the money into other asset classes, helping to fuel them.” Severe altcoin weakness “ultimately became a drag on BTC as well,” because it pushed people to “fully offramp from the crypto ecosystem, instead of taking profits into BTC.”

Looking ahead, his base case is quietly bearish on narratives and quietly constructive on time. Bitcoin “most likely” needs “a period of re-accumulation.” OG selling and quantum awareness will remain overhangs, while “gold and silver are cleaner and simpler bets on debasement.” Liquidity “may improve a lot if Trump successfully takes over the Fed,” but that is “a complex process, and half a year away.”

As of the end of 2025, in his telling, crypto underperformance is not a glitch – it is the logical outcome of who owns the coins, what they fear, and what the rest of the world chose to believe in instead.

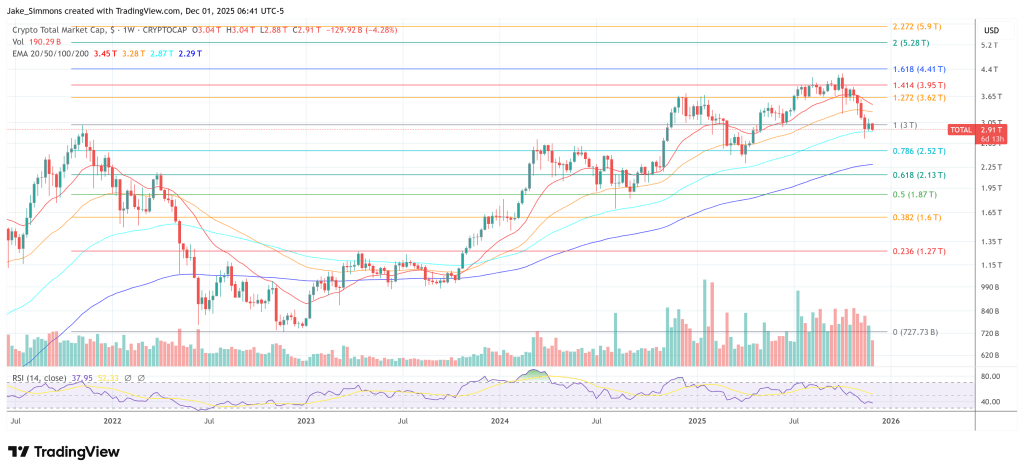

At press time, the total crypto market cap stood at $2.91 trillion.